“I think” is not an economic strategy. Yet too often, tax debates drift away from data and lived experience and toward short-term fixes that feel expedient in the moment. This week’s discussion in House Ways and Means around H.R.1 and selective decoupling from federal tax provisions puts Vermont at a familiar and consequential crossroads following testimony from an expert witness that emphasized professional judgment, with limited supporting data or publicly shared analysis available at the time of publication.

The issue before lawmakers is not whether Vermont faces fiscal pressure. It is whether the state continues a pattern of treating businesses as a fiscal backstop or chooses a path that strengthens affordability, predictability, and long-term economic stability.

The lived experience of Vermont employers is clear, and it is not theoretical. Business Climate Survey results consistently show that employers’ top challenges are workforce shortages, taxes and fees, and housing. These pressures are interconnected. When costs rise in one area, they compound strain across the entire system.

The overall business climate rating of 2.86 out of 5 captures that reality. Employers remain deeply committed to Vermont and their communities, but they are operating under rising costs, limited labor availability, and regulatory processes that often feel unpredictable or misaligned with economic conditions. That uncertainty is not academic. It directly affects business decisions.

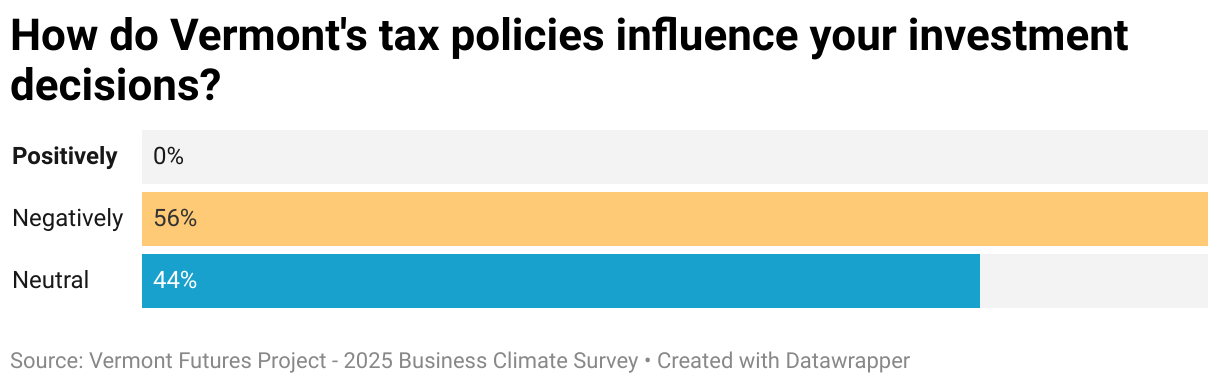

We see it clearly in investment behavior. More than one-third of Vermont employers anticipate making no investments in the next 12 months, while many others expect only minor investments. When asked how Vermont’s tax policies influence investment decisions, 56 percent say negatively, and zero percent say positively. This is not a signal to raise the cost of doing business. It is a warning that confidence is fragile and that policy narratives untethered from data carry real risk.

Opening and Closing Rates of Establishments (#45 out of 50)

This moment also deserves context. Just last year, lawmakers rightly expressed concern about the impact of federal tariffs on Vermont businesses. There was bipartisan recognition that when external forces raise costs and disrupt supply chains, state policy should not compound that harm. That same logic applies here. Selectively decoupling from federal tax provisions that support investment and innovation would stack new state-level costs on top of existing federal pressures, undercutting the very stability policymakers sought to preserve when tariffs hit.

Importantly, this is not a question of tax fairness or progressivity. Vermont already has one of the most progressive tax systems in the country, ranking near the top nationally according to the Institute on Taxation and Economic Policy. Thoughts that Vermont’s tax structure lacks progressivity are not supported by the data.

Table of ITEP Tax (In)equality Index (#3 out of 51)

The real issue is cost containment and fiscal discipline. Vermont ranks 46th nationally in state government spending per capita. At the same time, nearly two thirds of employers say public funds are not being used efficiently to support economic growth. That disconnect matters. Businesses are being asked to absorb higher costs without seeing corresponding improvements in affordability or outcomes.

Table of State Government Spending (#46 out of 50)

This is why proposals to decouple from federal provisions like R&D expensing are so concerning. Decoupling would raise the cost of innovation in Vermont relative to neighboring states, increase tax code complexity, and penalize firms investing in productivity, technology, and higher-wage jobs. In a state with a shrinking workforce, productivity-led growth is not optional. It is essential.

The Competitiveness Dashboard reinforces this point. Vermont ranks near the bottom nationally for business formation, investment momentum, and economic growth, while also ranking poorly on tax competitiveness. These are not isolated data points. They are signals of a system under strain that demand data-informed responses.

Table of Total Effective Business Tax Rate (#51 out of 51)

The outcome Vermont should be pursuing is clear. Tax policy should align with data and provide consistency when businesses face external shocks, whether from tariffs, interest rates, or labor constraints. Affordability will not be achieved through short-term tax decisions or by repeatedly targeting employers. It will come from bending the cost curve in healthcare and housing, controlling spending growth, and creating an environment where businesses feel confident investing for the long-term because policy decisions are anchored in evidence.

“I think” should not guide tax policy. The data already tells us what works. The choice now is whether Vermont is willing to follow it.